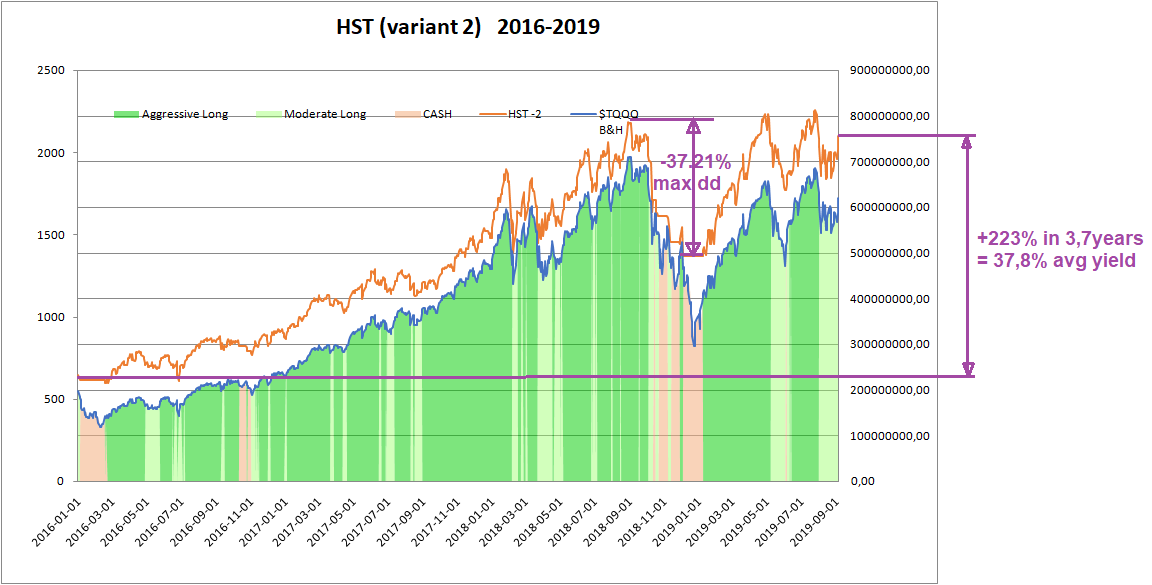

In our graphs published on StockTwits we show the performance of the HST model from 01-01-2016 to now = 3.7 years

It is interesting to notice that the average annual yield has been 37.8% for variant 2 (shifting among $TQQQ/$UPRO/Cash) and the max drawdown was suffered on Dec 2018 (-37.21% since previous top).

You see the ratio maxdd / avg yield is approx 1.0 which means that the model can suffer a drawdown very similar to the average annual yield...

..which also means that - on average - the HST model could recover a bad drawdown in approx ONE year

This is also the same ratio recorded from 1971 to now:

- max dd has been -54.6% (happened in 1998) and

- average annual yield has been 52.3%

So the ratio is again approx ~ 1.0 (this second picture is using log scale, so the drawdowns seem reduced than reality)

If one investor wants to reduce the MAGNITUDE of the max drawdown, should apply a less risky variant (i.e variant 5, using $SPY and $QQQ or others non-leveraged ETFs)