Can the HST model discriminate a temporary correction from a main correction or the start of a bear market?

This is a one-million dollar question, maybe more.

Truth is ....nobody knows.

Try writing the opinions of many gurus on the news, and check out one month later if/when they were right or wrong, you will discover that they are not better than flipping a coin.

The best we can do is make hypothesis, test them on long periods, and apply them on the future. This way, we have some chances to beat Buy&Hold.

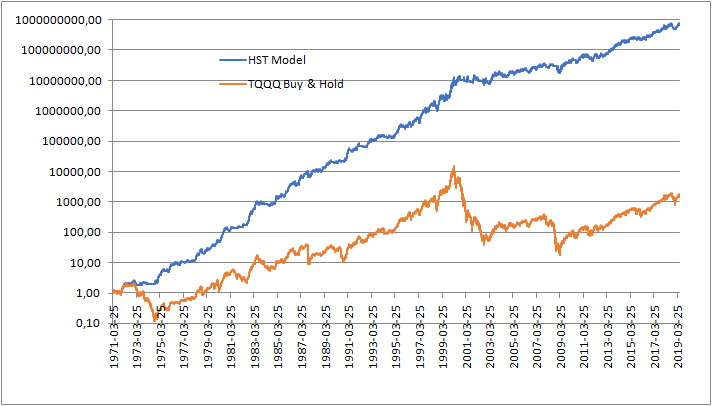

The HST model has been backtested on a huge period of 48 years, from 1971 (when the Nasdaq Composite index was born) to now, and has consistently succeeded in avoiding bear markets and big corrections, which happened in :

- 1973-1974

- 1981

- 1984

- 1986

- 1990

- 1994

- 2000-2002

- 2008

- 2011

- 2018

See the graph here: the orange line is simulating a 3x leveraged ETF based on Nasdaq (as TQQQ).

[Vertical axis is logaritmic in the first graph]

The Umbrella of HST model

Of these these negative years the HST model gave negative performances only in

Of these these negative years the HST model gave negative performances only in- 1973

- 1994

- 2002

- 2008

- 2011

- 2018

and losses has been completely manageable, and fully recovered few months later.

Read the article here.

Is there a crystal ball behind it? Not at all. Pure math: a mix of technical indicators and fundamental indicators.

Does the HST model avoid also minor corrections?

Sometimes it does, sometimes it doesn't. The HST model turns to cash usually when long-term technical indicators or economical indicators turn to negative.

But here is a typical behaviour of the market:

- economy is still good, no signs of bear markets or recession coming, but

- ... prices have gone up a bit too much, so

- ... a minor correction is pushing down prices to more appropriate levels

Jumping to cash every time a minor correction happens means damaging hardly the average yield of the model: there are too many false positives.

That's why the HST model is not yet bearish now (end of May 2019), when probably a correction is very close.

It will (automatically) turn to Cash, when there will be a confirmation of a high risk of bear market or main correction coming.

Still, I do not want to experience big losses, as - 40 / 50% from previous top. What can I do?

Very simple! Apply the HST model, but use non-leveraged ETFs.

The max drawdown in last 48 years was 22,3% and gave an annual average yield of 17,2% !